Easy Budgeting for the Modern Family

When you hear the word “budget”, do you cringe? I know I used to! It’s a bad word, full of responsibilities and adulting, am I right?! But in this day and age, budgeting is a very important aspect of your life as it can dictate everything that you do: what car you drive, where you take your vacations, even what you eat on a daily basis, etc.

After I graduated pharmacy school, I had my first “real” job and realized, “Oh man, there’s this money coming in. I have to make sure I’m allocating a certain amount to my living expenses, bills, school loans, and maybe a little bit to savings.” However, I had no idea if I was allocating enough to each thing. Is $500 a month a lot for groceries? Is $100 enough for gas? Having a category for each small thing was very confusing and frustrating. How can you possibly keep track of all that?

Enter in the 50/20/30 rule for budgeting. I stumbled upon this rule while on a Pinterest search and it has forever changed how I look at budgeting. Since then, I actually get excited about budgeting! I’m a nerd, I know. But now I know if I’m spending too much in one area and not enough in another. My financial goals are being met, we bought a house AND I paid off my $60k school loans in six years! Read on to see how the 50/20/30 rule works and how you can start applying it today with a free worksheet!

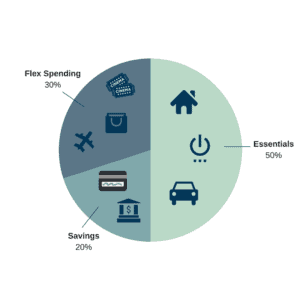

Fixed Costs – 50%

Half of your take-home pay (gross pay after income-based taxes, such as Federal/State tax) should be allocated to bills that do not vary from month to month. This includes rent/mortgage, car payment, and utilities. You can also include subscriptions such as gym memberships or Netflix since you are committed to paying the fee each month.

Financial Goals – 20%

After your essentials are taken care of (I mean, Netflix is essential, right? lol), you will now dedicate 20% of your take-home pay to your financial goals. This includes paying down credit card debt, building an emergency fund, or saving for retirement. You may have other financial goals, including a down payment for a house or repaying student loans. An important aspect of this budgeting rule is that you “pay yourself first” before having fun with the leftover money.

Flexible Spending – 30%

So you’ve taken care of your essentials and working on your financial goals. Finally, the last 30% of your take-home can now be dedicated to your flexible spending. This includes day-to-day expenses that may vary from month to month, such as groceries, gas, shopping, entertainment, eating out, etc. You do not need to have a specific budget for each of these expenses, but be aware of your spending and do not go over your flex spending budget. For example, you may eat out more one month and not as much the next month, but you can be flexible in the other areas of spending to ensure that you are not going over 30%.

And that’s it! A very simple and easy budgeting rule. Hopefully, you didn’t just cringe at the word “budget”. 🙂 Are you ready to put this rule into action? Download this free worksheet, plug in your budget items and numbers and you’ll be set! How do you budget now? I would love to hear other ideas. If you try this rule, let me know how it works for you! Happy budgeting!

[maxbutton id=”1″ url=”https://docs.google.com/spreadsheets/d/18Jzbq-rumZWs5YaZt2cOeuE7Ph8Tvcl9xBiUtkynpcI/edit?usp=sharing” ]